Challenge: Strategic Investment Dilemmas for Future Payment Methods

Deciding where to invest internal resources for future payment methods is a complex strategic challenge. Merchants face the dilemma of whether to invest in substantial infrastructure to fix current payment method issues (like EFT CX) or to “hedge bets” on emerging technologies like PayShap. There’s uncertainty about how quickly new technologies will scale, and if customers will even understand them, potentially requiring additional education efforts. Investing in features customers don’t yet know or trust adds another layer of complexity.

How a Tailored Partner Solves This:

A specialised payment partner like us with deep local market knowledge is crucial for navigating these investment decisions. They can help assess market readiness and potential adoption rates for new technologies. For instance, African Payment Solutions (APS) has already implemented Visa network tokenization (being the second in South Africa to do so) and is working on Mastercard tokenization (aiming to be the first or second). This technology offers “a lot of benefits for the e-commerce merchant”, demonstrating a proactive approach to integrating future-proof payment solutions that benefit merchants.

“When coming across headlines about African payments, leapfrogging is used as a description, which implies that Africa is catching up. In many ways, Africa is on its own path and some of what we’re doing is ahead of what is being done in Europe or the US. Our path is also not to replicate what is being done in Europe or the US. Payments have been instant across Sub-Saharan Africa since 2010.” – Dare Okoudjou, founder and CEO of MFS Africa.

Africa is Informal

The vast majority of spending in Africa takes place in informal markets that remain overlooked by traditional measures. The modern retail channel only accounts for 10% of the total retailing value in the region, to the extent that it is more accurate to refer to these informal markets as the Main Market sector.

Africa is Mobile

Africans are early adopters of mobile money – more than half of global mobile-money service operators are located in Sub-Saharan Africa. The continent has the highest unbanked population in the world, the fastest growing population, and the highest proportion of microbusinesses. Mobile phones are the main source of access to the Internet for young consumers in Africa and in 2020, transactions on mobile money platforms reached $490 billion, a trend that the covid pandemic has hastened.

Mobile payments are also accelerating in the ecommerce environment, and is predicted to be the driving force behind digital transformation in payments globally over the next five years. The digital payments market has matured faster in Africa than it has in Europe: The number of electronic payment transactions in Nigeria grew from 66 million in 2008 to over two billion in 2018. By way of example, the number of electronic payments in France has grown in the past decade, from 33 million in 2009 to only 61.5 million in 2018.

However, mobile payments are not able to transact cross-jurisdictionally and so limits growth of African commerce into global markets.

Africa is Crypto

At the same time, the Sub-Saharan region has the largest volume of retail transactions in crypto (defined as less than USD10,000) and remittances from abroad, and despite a recent ban on crypto in Nigeria, transaction volumes were unchanged.

The bottom line:

Looking at these three trends, we predict that as an electronic, peer-to-peer, universally accessible currency, crypto holds particular promise to catapult Africans into a truly globally competitive and accessible e-commerce era.

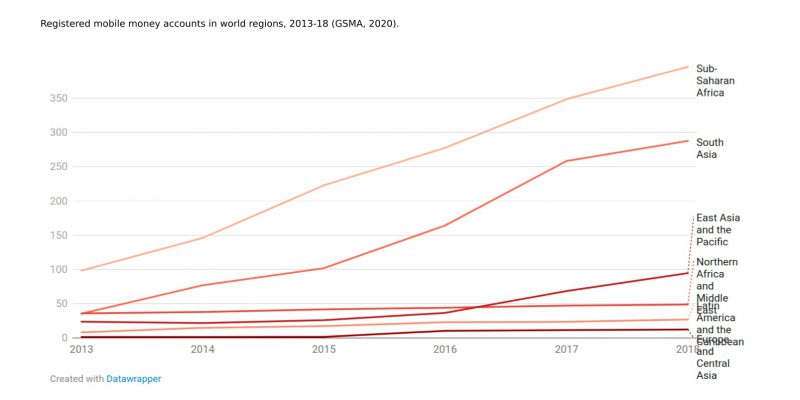

Graph: Registered mobile money accounts in world regions, 2013-18 (GSMA, 2020).

About the authors

Bernobin is BERNelle and rOBIN’s adventures in online payments, crypto and the metaverse.

This thought piece was written as part of Robin Philip’s Masters research in Digital Currency, to update his 20 years experience in online payments. As co-founder of African Payment Solutions, a pan-African eCommerce payments company for multinational eCommerce merchants, he is considering how to best serve clients in the rapidly evolving future of ecommerce.

Bernelle Verster is trained as a bioprocess engineer, and recently changed gear to explore 3D geospatial and data visualisation, with great excitement for the metaverse. Her interest is in interfaces, the spaces between: How we transition responsibly to a decentralised … more democratic?, more digital way of doing things? How does that link back to the physical world? How do we empower people who have thus far been excluded from the dominant economic forces?

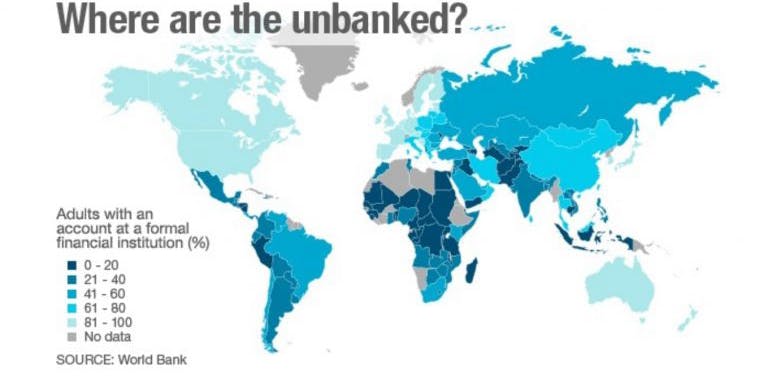

60% of Africa’s population (17% of the world’s unbanked) do not participate in the formal banking system.

Only 35% of Africans (456 million adults of a total population estimated at 1.3 billion) were expected to have a bank account by 2022.

40 million Europeans are unbanked, and we can only guess how many are venturing into having a digital identity completely independent of the formal network.

Conventional thinking surmises that the unbanked are being left behind, are too poor, or do not have the knowledge or other resources to participate in the formal banking sector.

Or, is it perhaps because it is simply not worth the hassle?

Traditional banking runs on dated banking models of branch networks, expensive technology, inadequate systems and a limited talent pool. In the aftermath of a global financial crisis and the covid pandemic, the promise that “formal financial services can help people to protect their earnings, and participate in economic activities” is losing its appeal.

Could it be that poor people knew this all along, and the rest of us are only now catching up?

The adoption of cryptocurrency infrastructure is driven by perceived failings of traditional financial systems and distrust in governments. Mistrust and governance issues aside, microbusiness and informal markets don’t want to be hamstrung by bureaucracy. South Africa, Kenya and Nigeria are in the top 10 countries of highest grassroots crypto adoption in the world.

The sluggish, inefficient and not customer-minded banking sector may be a tolerable inconvenience for higher earners, but it is simply not good enough for the micro-enterprises making up the bulk of Sub-Saharan Africa’s economic activity.

Supported by design

Innovation in banking services is not necessarily choosing between the traditional banking system or the emerging and currently poorly regulated crypto scene. Can formal banking improve, be more accommodating to their clients’ needs? Improved service targeting the lower income brackets include updating their technology and infrastructure systems, and updating their KYC requirements to be less burdensome. This may mean introducing smart contracts, digital assets and the efficiencies of technologies currently associated with crypto. If they don’t, more and more people will take the risk on crypto.

At the same time, regulators need to be more open minded and embracing of the efficiencies and economic benefits of DeFi’s fast, pseudonomous, borderless payments starting with lower amounts or lower risk areas.

Over the past year, a record number of new accounts have been opened worldwide by firms providing mobile money, fintech and online banking services. Following the pandemic, more people are leaving the formal economy. Crypto makes it possible and more efficient. Two aspects are catalysts to this migration: Peer to peer (P2P) platforms and layer two technologies.

P2P platforms are essential to service adoption in developing countries and are particularly suited to unbanked individuals. P2P platforms don’t custody any of the digital assets or fiat traded on their platforms, negating the need to connect to the banking system and comply with strenuous regulatory hurdles. This allows them to onboard residents of developing countries more easily, many of whom are excluded from the traditional financial ecosystem.

Layer two technologies are ‘off-chain’ protocols that do not record every single transaction on the bitcoin blockchain. These protocols, like the Lightning network, are effectively independent of the value of Bitcoin thus avoiding the risk of the crypto volatility. In short, layer two technologies enable very cheap, very fast transactions.

It would be prudent for African banks and governments to catch up with this runaway train of a more efficient mechanism of decentralised, borderless money as a store of value and medium of exchange. Embracing these new monetary technologies can give Africa and Africans a global competitive advantage. The genie is out of the bottle.

Further reading:

www.gfmag.com

www.paymentscardsandmobile.com

www.elixirr.com

www.wsbi-esbg.org

repository.uel.ac.uk

link.springer.com

go.chainalysis.com

About the authors

This thought piece, the second in the series, was written as part of Robin Philip’s Masters research in Digital Currency, to update his 20 years experience in online payments. As co-founder of African Payment Solutions, a pan-African eCommerce payments company for multinational eCommerce merchants, he is considering how to best serve clients in the rapidly evolving future of ecommerce.

Bernelle Verster is trained as a bioprocess engineer, and recently changed gear to explore 3D geospatial and data visualisation, with great excitement for the metaverse. Her interest is in interfaces, the spaces between: How do we transition responsibly to a decentralised … more democratic?, more digital way of doing things? How does that link back to the physical world? How do we empower people who have thus far been excluded from the dominant economic forces?

Local institutions are familiar with local payments market. Local SME’s are growing fast and require a lot of attention and support. Incoming digital commerce can benefit from local legal entity, local compliance, local forex management, protection from the vagaries of internet connectivity, culture, language, legacy systems, local knowledge, local infrastructural instability . . so this is where we can help. Not just a payment provider but as an enabler.

African is a big consumer market with low ATV’s. There are big opportunities for sharing platforms, digital and especially entertainment with COVID, transport and logistics platforms (also COVID-inspired) and a wild card is insurance.

Also successful African eCommerce merchnats seem to have limited understanding and capabilities to set up effective global acquiring for example in Europe and the UK.

Into Africa is card, mobile and EFT and cross border to Europe is mainly card.

The ability for multinational, eCommerce companies in UK and Europe to deal with someone from their home region with African roots makes a difference to their level of understanding and trust levels. In-country acquirers like to deal with their own people and so it works with us having locals on the ground in each country.

The APS strategy of small staff requires a level of outsourcing non-core elements and the choice of leverable business opportunities that require low but very experienced input and value add in exchange for a higher return

So if you are looking for payment at the checkout, and want a team that is very experienced in online payments, click here to give us a shout

International businesses have the volume and and are looking for a minimum level of certainty and risk management when it comes to acquiring across the continent. Most non-African merchants and payment providers expect African acquiring and payments to be like more developed markets, but it’s not.

It is imperative that the key payment methods of each territory need to be supported. The further out one goes to less developed countries, the higher need for smoothing out the experience for multinational merchants.

Card acquiring can be done from abroad, but the conversion rates will be a lot lower. Many international issuing banks are blocking acquiring by African banks, and acquiring banks block transactions involving African issued cards.

There seems to be few companies offering the “single API” and “all payment methods with local conditions taken care of”.

This job will become easier over time as a result of interoperability initiatives like Hover, Mojaloop, Mowali and the mobile payment aggregators like MFS. But they are all in the embryo stages and will need a lot of completion and maturing.

Some of the local payment platforms going multiregional have been experiencing quality delivery problems as a consequence of their scaling.

It is imperative that we at APS continue to deliver smooth operations and service delivery to our multinational, target market whilst taking care of the inconsistencies and anomalies of the African market.