“When coming across headlines about African payments, leapfrogging is used as a description, which implies that Africa is catching up. In many ways, Africa is on its own path and some of what we’re doing is ahead of what is being done in Europe or the US. Our path is also not to replicate what is being done in Europe or the US. Payments have been instant across Sub-Saharan Africa since 2010.” – Dare Okoudjou, founder and CEO of MFS Africa.

Africa is Informal

The vast majority of spending in Africa takes place in informal markets that remain overlooked by traditional measures. The modern retail channel only accounts for 10% of the total retailing value in the region, to the extent that it is more accurate to refer to these informal markets as the Main Market sector.

Africa is Mobile

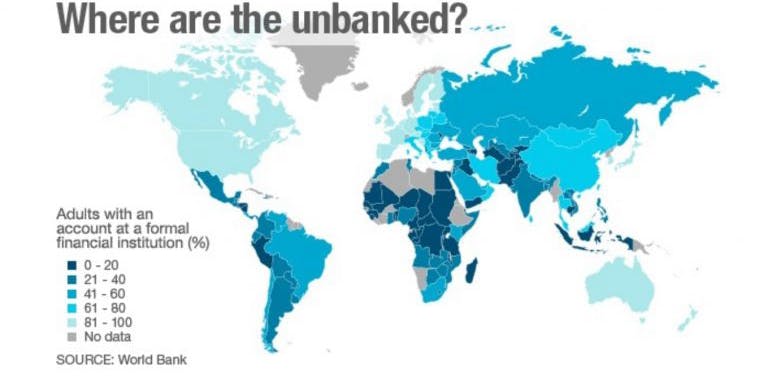

Africans are early adopters of mobile money – more than half of global mobile-money service operators are located in Sub-Saharan Africa. The continent has the highest unbanked population in the world, the fastest growing population, and the highest proportion of microbusinesses. Mobile phones are the main source of access to the Internet for young consumers in Africa and in 2020, transactions on mobile money platforms reached $490 billion, a trend that the covid pandemic has hastened.

Mobile payments are also accelerating in the ecommerce environment, and is predicted to be the driving force behind digital transformation in payments globally over the next five years. The digital payments market has matured faster in Africa than it has in Europe: The number of electronic payment transactions in Nigeria grew from 66 million in 2008 to over two billion in 2018. By way of example, the number of electronic payments in France has grown in the past decade, from 33 million in 2009 to only 61.5 million in 2018.

However, mobile payments are not able to transact cross-jurisdictionally and so limits growth of African commerce into global markets.

Africa is Crypto

At the same time, the Sub-Saharan region has the largest volume of retail transactions in crypto (defined as less than USD10,000) and remittances from abroad, and despite a recent ban on crypto in Nigeria, transaction volumes were unchanged.

The bottom line:

Looking at these three trends, we predict that as an electronic, peer-to-peer, universally accessible currency, crypto holds particular promise to catapult Africans into a truly globally competitive and accessible e-commerce era.

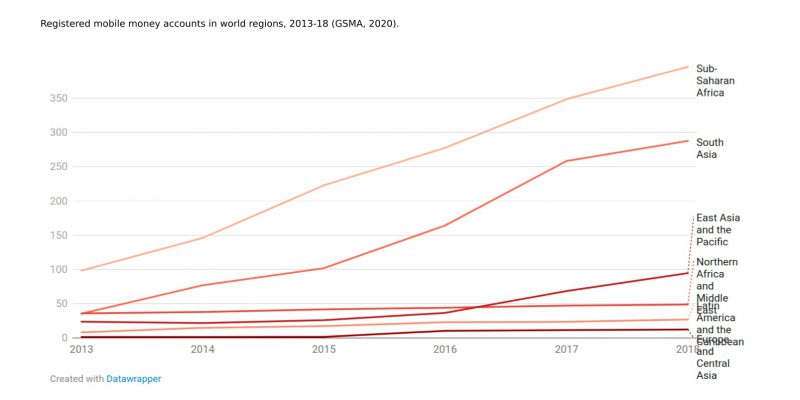

Graph: Registered mobile money accounts in world regions, 2013-18 (GSMA, 2020).

About the authors

Bernobin is BERNelle and rOBIN’s adventures in online payments, crypto and the metaverse.

This thought piece was written as part of Robin Philip’s Masters research in Digital Currency, to update his 20 years experience in online payments. As co-founder of African Payment Solutions, a pan-African eCommerce payments company for multinational eCommerce merchants, he is considering how to best serve clients in the rapidly evolving future of ecommerce.

Bernelle Verster is trained as a bioprocess engineer, and recently changed gear to explore 3D geospatial and data visualisation, with great excitement for the metaverse. Her interest is in interfaces, the spaces between: How we transition responsibly to a decentralised … more democratic?, more digital way of doing things? How does that link back to the physical world? How do we empower people who have thus far been excluded from the dominant economic forces?

Further reading:

- https:///thepaypers.com/expert-opinion/mobile-payments-key-market-developments–1251382

- https://www.gsma.com/mobileeconomy/wp-content/uploads/2021/09/GSMA_ME_SSA_2021_English_Web_Singles.pdf

- https://www.giz.de/expertise/downloads/Blockchain in Africa.pdf

- https://corporateandinvestment.standardbank.com/static_file/CIB/PDF/2020/Sectors/Africa_Consumer_Insight_Report.pdf

- https://www.finextra.com/the-long-read/44/there-is-more-to-digital-payments-in-africa-than-m-pesa

- https://go.chainalysis.com/rs/503-FAP-074/images/2020-Geography-of-Crypto.pdf

- https://qz.com/africa/2125096/what-would-it-take-to-lift-nigerias-cryptocurrency-ban/