Insight for eCommerce merchants in Africa: Catering to local payment preferences is crucial for success. Millions of African consumers prefer and utilise in-country local payment methods. Diverse pan-African payment options include Credit Cards, Debit Cards, and popular mobile money solutions like M-PESA. By providing these familiar and trusted payment methods, you can significantly expand your reach and conversion rates.

The digital marketplace continues its relentless evolution, and as we look towards 2025, several key trends are poised to reshape how we buy and sell online. These shifts will have profound implications globally, and particularly within the dynamic landscape of African marketplaces. Let’s delve into the major forces at play and consider their potential impact.

One of the most significant trends highlighted across the sources is the rise of Embedded Finance. Marketplaces are increasingly looking to integrate financial services directly into their platforms, moving beyond simply facilitating transactions. This includes offerings like in-platform lending, insurance, investment options for sellers, and even Buy Now, Pay Later (BNPL) solutions. This is particularly relevant for African marketplaces, where access to traditional financial services may be limited. The integration of such features can foster greater financial inclusion, enabling both merchants and consumers in smaller towns and rural areas to participate more actively in the digital economy. Wallet-driven ecosystems, as suggested by Francesc Altisent from Mangopay, could be instrumental in delivering these embedded services seamlessly within the marketplace interface.

Another powerful force shaping the future is Artificial Intelligence (AI)-driven personalisation and automation. From enhancing product recommendations and customer service to optimising checkout experiences and detecting fraud, AI is set to become even more pivotal. Abdesselam Benzitouni of Jumia notes that consumers expect more personalised shopping experiences, and marketplaces leveraging AI for this will gain a competitive edge. For African marketplaces, AI can help overcome logistical challenges and cater to diverse consumer needs across vast geographical areas. AI-powered personalisation can also make online shopping more appealing and relevant to local preferences. However, Marius Galdikas, CEO at ConnectPay, cautions about the immediate transformative impact of AI due to the energy requirements and regulatory unease around its “black box” nature.

The demand for seamless and instant payouts is also a growing trend. As platforms compete for user trust and engagement, integrating instant, frictionless transactions will become a critical differentiator. Max Lehmann from Nium highlights that business sellers, regardless of location, will expect instant cross-border payments. While the lack of common global payment rails currently makes closed-loop systems attractive for faster, reliable transfers, the increasing adoption of real-time payment infrastructures across regions could change this. For African marketplaces facilitating cross-border trade or serving sellers in remote areas, efficient payout mechanisms are crucial for building trust and encouraging participation.

Hyper-local commerce is identified as an increasingly important aspect. Consumers are looking for more locally relevant experiences, and marketplaces that can cater to these needs will likely thrive. Irene Skrynova from Unlimit also points to hyper-personalisation as redefining marketplace payments. Abdesselam Benzitouni of Jumia specifically mentions that the marketplace economy in 2025 will be increasingly shaped by hyper-local commerce. This trend aligns well with the diverse and localized nature of many African markets. Marketplaces that can effectively connect local buyers and sellers and offer tailored services will be well-positioned for growth.

The rise of social commerce will also continue to redefine how consumers interact with brands and make buying decisions. Platforms will increasingly integrate seamless in-app shopping experiences. Emre Talay from Payrails notes that social commerce is reshaping how people discover and transact. African marketplaces can leverage the widespread use of social media across the continent to tap into new customer bases and create more engaging shopping experiences.

Cross-border growth remains a significant revolution in the marketplace economy. Maria Parpou from Mastercard Gateway states that a staggering 75% of cross-border transactions occur through marketplaces, and this percentage is expected to rise. To remain competitive, marketplaces must expand their payment methods to include local wallets and domestic schemes. For African marketplaces, this presents both opportunities and challenges. The ability to facilitate seamless cross-border transactions can unlock access to larger markets and a wider range of products. However, it also necessitates navigating diverse payment landscapes and regulatory environments.

It’s important to note the increasing focus on infrastructure and the potential for increased competition. Marketplaces are moving towards more flexible setups with multi-acquirer options and local payment methods. At the same time, heightened competition could lead to higher user acquisition costs. Dorota Wróbel from G2A.COM suggests that value-added services for both sellers and buyers will be key differentiators. African marketplaces will need to focus on building robust and adaptable infrastructures while also offering unique value propositions to stand out in a potentially crowded space.

Finally, the importance of digital payments and financial inclusion cannot be overstated, particularly in the African context. Mobile wallets, BNPL solutions, and alternative payment methods are already driving more online transactions in smaller towns and rural areas. This trend is likely to continue, and marketplaces that can effectively cater to these diverse payment preferences will be better positioned for success.

In conclusion, the marketplace economy in 2025 will be characterised by embedded finance, AI-driven personalisation, seamless payments, a focus on local needs, the integration of social commerce, and continued cross-border expansion. For African marketplaces, these trends present significant opportunities to enhance financial inclusion, cater to diverse consumer preferences, and facilitate both local and international trade. However, navigating regulatory landscapes, building robust infrastructure, and differentiating themselves in a competitive environment will be crucial for sustained growth and impact.

In today’s digital marketplace, offering a secure and smooth online shopping experience is vital. Tokenisation is a game-changing technology that’s enhancing online payments. Here are the top 5 advantages for your eCommerce business:

Ramp Up Security and Slash Fraud: Tokenisation swaps sensitive card data (PAN) for unique, random tokens. These tokens are useless to cybercriminals, significantly reducing your risk of data breaches. Tokenisation can cut card-not-present (CNP) fraud by up to 26% and averages a 30% reduction online compared to using PANs. This builds customer trust and protects your bottom line.

Unlock Higher Authorisation Rates for More Sales: Tokenised transactions often see improved authorisation rates because they can provide issuers with richer data. Visa data indicates an average 3% increase in authorisation rates for CNP transactions using tokens. Bolt experienced token authorisation rates of 95.9% versus 90.8% for PANs. This means fewer failed transactions and more completed sales.

Delight Customers with Effortless Checkout: Tokenisation enables one-click checkout for returning customers thanks to card-on-file tokens. What’s more, automatic updates of tokenised card details for expired or replaced cards ensure uninterrupted service for subscriptions and recurring payments. This smoother experience leads to less cart abandonment and happier, more loyal customers.

Simplify Operations with Automated Lifecycle Management: Managing outdated card details can be a headache. Tokenisation automates this process with issuers updating token details in the background when cards expire or are replaced. This reduces the need to chase customers for new information and streamlines your operations.

Trim PCI DSS Scope and Costs: The PCI DSS demands strict security for handling cardholder data. By adopting tokenisation and avoiding the storage of actual PAN data, you can potentially significantly reduce your PCI DSS compliance burden, costs, and complexity. This frees up resources to focus on growing your business.

Considering the ever-increasing sophistication of online fraud and the demand for seamless online shopping, how confident are you that your current payment system is fully optimised to safeguard your business and maximise your sales conversions?

“When coming across headlines about African payments, leapfrogging is used as a description, which implies that Africa is catching up. In many ways, Africa is on its own path and some of what we’re doing is ahead of what is being done in Europe or the US. Our path is also not to replicate what is being done in Europe or the US. Payments have been instant across Sub-Saharan Africa since 2010.” – Dare Okoudjou, founder and CEO of MFS Africa.

Africa is Informal

The vast majority of spending in Africa takes place in informal markets that remain overlooked by traditional measures. The modern retail channel only accounts for 10% of the total retailing value in the region, to the extent that it is more accurate to refer to these informal markets as the Main Market sector.

Africa is Mobile

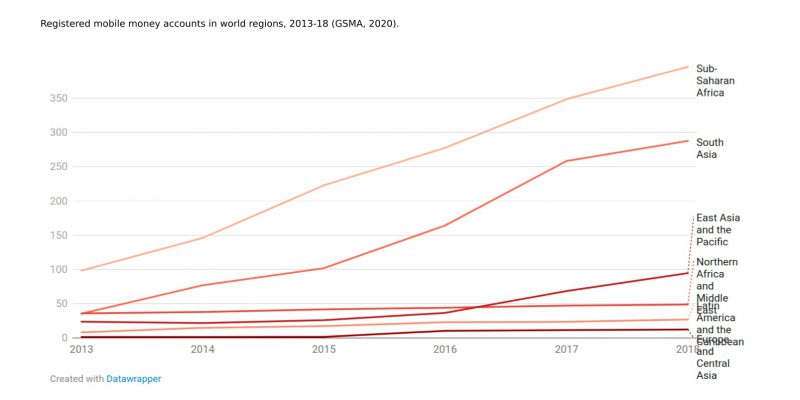

Africans are early adopters of mobile money – more than half of global mobile-money service operators are located in Sub-Saharan Africa. The continent has the highest unbanked population in the world, the fastest growing population, and the highest proportion of microbusinesses. Mobile phones are the main source of access to the Internet for young consumers in Africa and in 2020, transactions on mobile money platforms reached $490 billion, a trend that the covid pandemic has hastened.

Mobile payments are also accelerating in the ecommerce environment, and is predicted to be the driving force behind digital transformation in payments globally over the next five years. The digital payments market has matured faster in Africa than it has in Europe: The number of electronic payment transactions in Nigeria grew from 66 million in 2008 to over two billion in 2018. By way of example, the number of electronic payments in France has grown in the past decade, from 33 million in 2009 to only 61.5 million in 2018.

However, mobile payments are not able to transact cross-jurisdictionally and so limits growth of African commerce into global markets.

Africa is Crypto

At the same time, the Sub-Saharan region has the largest volume of retail transactions in crypto (defined as less than USD10,000) and remittances from abroad, and despite a recent ban on crypto in Nigeria, transaction volumes were unchanged.

The bottom line:

Looking at these three trends, we predict that as an electronic, peer-to-peer, universally accessible currency, crypto holds particular promise to catapult Africans into a truly globally competitive and accessible e-commerce era.

Graph: Registered mobile money accounts in world regions, 2013-18 (GSMA, 2020).

About the authors

Bernobin is BERNelle and rOBIN’s adventures in online payments, crypto and the metaverse.

This thought piece was written as part of Robin Philip’s Masters research in Digital Currency, to update his 20 years experience in online payments. As co-founder of African Payment Solutions, a pan-African eCommerce payments company for multinational eCommerce merchants, he is considering how to best serve clients in the rapidly evolving future of ecommerce.

Bernelle Verster is trained as a bioprocess engineer, and recently changed gear to explore 3D geospatial and data visualisation, with great excitement for the metaverse. Her interest is in interfaces, the spaces between: How we transition responsibly to a decentralised … more democratic?, more digital way of doing things? How does that link back to the physical world? How do we empower people who have thus far been excluded from the dominant economic forces?

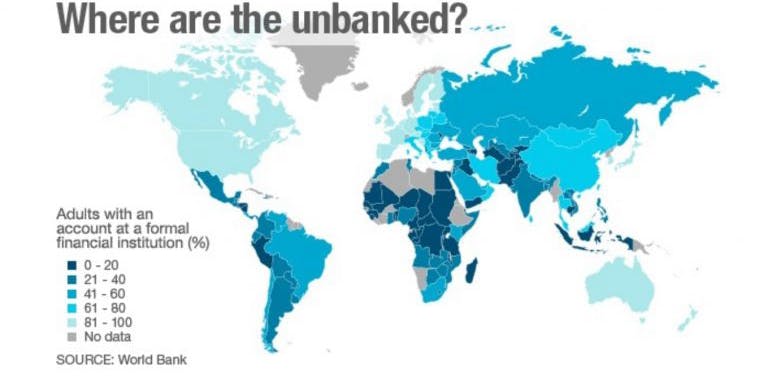

60% of Africa’s population (17% of the world’s unbanked) do not participate in the formal banking system.

Only 35% of Africans (456 million adults of a total population estimated at 1.3 billion) were expected to have a bank account by 2022.

40 million Europeans are unbanked, and we can only guess how many are venturing into having a digital identity completely independent of the formal network.

Conventional thinking surmises that the unbanked are being left behind, are too poor, or do not have the knowledge or other resources to participate in the formal banking sector.

Or, is it perhaps because it is simply not worth the hassle?

Traditional banking runs on dated banking models of branch networks, expensive technology, inadequate systems and a limited talent pool. In the aftermath of a global financial crisis and the covid pandemic, the promise that “formal financial services can help people to protect their earnings, and participate in economic activities” is losing its appeal.

Could it be that poor people knew this all along, and the rest of us are only now catching up?

The adoption of cryptocurrency infrastructure is driven by perceived failings of traditional financial systems and distrust in governments. Mistrust and governance issues aside, microbusiness and informal markets don’t want to be hamstrung by bureaucracy. South Africa, Kenya and Nigeria are in the top 10 countries of highest grassroots crypto adoption in the world.

The sluggish, inefficient and not customer-minded banking sector may be a tolerable inconvenience for higher earners, but it is simply not good enough for the micro-enterprises making up the bulk of Sub-Saharan Africa’s economic activity.

Supported by design

Innovation in banking services is not necessarily choosing between the traditional banking system or the emerging and currently poorly regulated crypto scene. Can formal banking improve, be more accommodating to their clients’ needs? Improved service targeting the lower income brackets include updating their technology and infrastructure systems, and updating their KYC requirements to be less burdensome. This may mean introducing smart contracts, digital assets and the efficiencies of technologies currently associated with crypto. If they don’t, more and more people will take the risk on crypto.

At the same time, regulators need to be more open minded and embracing of the efficiencies and economic benefits of DeFi’s fast, pseudonomous, borderless payments starting with lower amounts or lower risk areas.

Over the past year, a record number of new accounts have been opened worldwide by firms providing mobile money, fintech and online banking services. Following the pandemic, more people are leaving the formal economy. Crypto makes it possible and more efficient. Two aspects are catalysts to this migration: Peer to peer (P2P) platforms and layer two technologies.

P2P platforms are essential to service adoption in developing countries and are particularly suited to unbanked individuals. P2P platforms don’t custody any of the digital assets or fiat traded on their platforms, negating the need to connect to the banking system and comply with strenuous regulatory hurdles. This allows them to onboard residents of developing countries more easily, many of whom are excluded from the traditional financial ecosystem.

Layer two technologies are ‘off-chain’ protocols that do not record every single transaction on the bitcoin blockchain. These protocols, like the Lightning network, are effectively independent of the value of Bitcoin thus avoiding the risk of the crypto volatility. In short, layer two technologies enable very cheap, very fast transactions.

It would be prudent for African banks and governments to catch up with this runaway train of a more efficient mechanism of decentralised, borderless money as a store of value and medium of exchange. Embracing these new monetary technologies can give Africa and Africans a global competitive advantage. The genie is out of the bottle.

Further reading:

www.gfmag.com

www.paymentscardsandmobile.com

www.elixirr.com

www.wsbi-esbg.org

repository.uel.ac.uk

link.springer.com

go.chainalysis.com

About the authors

This thought piece, the second in the series, was written as part of Robin Philip’s Masters research in Digital Currency, to update his 20 years experience in online payments. As co-founder of African Payment Solutions, a pan-African eCommerce payments company for multinational eCommerce merchants, he is considering how to best serve clients in the rapidly evolving future of ecommerce.

Bernelle Verster is trained as a bioprocess engineer, and recently changed gear to explore 3D geospatial and data visualisation, with great excitement for the metaverse. Her interest is in interfaces, the spaces between: How do we transition responsibly to a decentralised … more democratic?, more digital way of doing things? How does that link back to the physical world? How do we empower people who have thus far been excluded from the dominant economic forces?

Notes for video: Kalon Venture Partners . . introduced to me to the term COVID-beneficiaries.

Platforms and marketplaces, particularly related to core growth opportunities, like historically tourism and travel, and into the future SME’s moving their services online, and the consequent demand for transport and logistics systems

Opportunity – Incoming platforms moving from mature markets to underserved markets across Africa is a sweet spot. They need all the help they can get and they have better margins and investment capability to tackle the market en masse to gain market share right now with smooth payment services taken care of. This is particularly relevant when it comes to COVID-beneficiary businesses who are significantly benefitting from the new way of being.

These verticals will be on a growth curve into the future: Retail and particularly essential services; tourism and travel will come back on stream but it will take some time – and Africa is most likely down the list when it comes to international tourism and travel operators looking for places to book and pay.

Home entertainment like Netflix, Amazon Prime, PayTV, betting, gambling and gaming are high growth markets. To facilitate eCommerce deliveries and to bridge the gap between people, logistics and delivery companies are thriving.

Think about your business and who it is serving and which of those or potentially new ones are onto a good growth curve.

eCommerce was on a strong growth curve before, and COVID has been rocketfuel for existing and effectively all businesses who are woke enough to move their services online.

If we follow the premise that a largely informal, mobile world is well suited to the digital finance revolution, and that people choose to be unbanked, then the next step is to explore how best to support the need to interface between fiat and crypto.

This need is created by two challenges: low discretionary spending power and high transaction fees.

People in the $5-$10 consumption/day income band hold the highest concentration of discretionary spending power on the African continent. Their transaction values are typically also small, classified as retail transactions (defined as less than USD10,000). Hence, a first step to facilitate financial innovation is to focus on low risk, small amounts, similar to what effectively could be cross-border mobile money. Remittances are of particular relevance here, but the ability to get paid for services from anywhere in the world promises particular service driven economic growth. In other words, providing a geography-independent means to supplement income.

Remittances below $200 between two Sub-Saharan African countries cost an average of 9% in fees, compared to the global average of 6.8%. For some country pairs that see large remittance flows, such as South African to Nigeria or South Africa to Malawi, the fees can be as high as 15%. Sub-Saharan Africa remains the most expensive region to send money to, recorded at 7.83 percent total average cost in Q4 2021.

Banks remain the most expensive type of service provider, with an average cost of 10.44 percent.

It then comes as no surprise that the Sub-Saharan region has the largest volume of retail transactions using cryptocurrency. But the challenge of on-chain Bitcoin for poor people is the volatility of the currency and higher fees of on-chain activity. The utility of crypto is its geographic independence. The lightning network, however, takes a slightly different approach.

The Lightning Network

At this point it is important to make the distinction between bitcoin, the asset class, and the global interoperable bitcoin monetary network. The Lightning Network is built off the latter, and enables people to seamlessly go between bitcoin and a fiat-backed stablecoin. And they can send those globally, instantly and with extremely low fees. Think of it as a hybrid of the SWIFT financial messaging system (the communication layer) and correspondent banking (routing component).

People are quietly taking notice. Bitcoin Trade Namibia, a non-custodial Bitcoin ‘on/off-ramp’ service based in Namibia, is now processing 80% of its volume over the Lightning Network as of April 2021. Emerging markets are increasingly showing huge adoptions due to instant low bitcoin transactions.

r/Bitcoin – Bitcoin Lightning Network used in South Africa 3,649 votes and 302 comments so far on Reddit www.reddit.comThere’s a new way to quickly send U.S. dollars around the world with bitcoin Lightning Labs announced it’s launching the Taro protocol that will route stablecoins and other digital assets through the bitcoin monetary network. www.cnbc.com80% of Bitcoin Trade Namibia On/Off-Ramp Volumes Are Now via The Lightning Network as of April 2021 – BitcoinKE The Bitcoin Lightning network has seen explosive growth in 2021 as the number of channels, channel values, and nodes, increased exponentially in Q1, 2021. According to the latest reports, Bitcoin Trade Namibia, a non-custodial Bitcoin ‘on/off-ramp’ service based in Namibia, is now processing 80% of… bitcoinke.ioLightning Labs raises funding to enable stablecoin transfers through Bitcoin network – TechCrunch Lightning Labs raises funds from Robinhood CEO, others to enable stablecoin transactions through Bitcoin network techcrunch.com

About the authors

This thought piece, the third in the series, was written as part of Robin Philip’s Masters research in Digital Currency, to update his 20 years experience in online payments. As co-founder of African Payment Solutions, a pan-African eCommerce payments company for multinational eCommerce merchants, he is considering how to best serve clients in the rapidly evolving future of ecommerce.

Bernelle Verster is trained as a bioprocess engineer, and recently changed gear to explore 3D geospatial and data visualisation, with great excitement for the metaverse – or the immersive internet. Her interest is in interfaces, the spaces between: How do we transition responsibly to a decentralised … more democratic?, more digital way of doing things? How does that link back to the physical world? How do we empower people who have thus far been excluded from the dominant economic forces?

Vertical potentials & opportunities across Sub-Saharan Africa for Multinational eCommerce Companies

Vertical potentials and opportunities?

Retail – giant size eCommerce (for eg Takealot, Jumia, Safaricom’s Masoko) are mostly well advanced when it comes to their own payments systems. The silver lining is that this is paving the way for international eCommerce companies to leverage the improved consumer education, logistics and payment systems

Tourism and Travel – Tourism and travel are a key contributor to GDP in many SSA countries and booking engines through aggregation provide good payment opportunities

Betting and Gambling – digital and accessible, not affected by lack of infrastructure, and popular for entertainment

Deliveries and Ridesharing – transport is a base layer for all economies across SSA and the relatively underdeveloped transport infrastructures provide ample opportunities for private service provision off aggregator platforms

PayTV – the growth in PayTV has been significant, with Multichoice paving the way for other providers and runner up Netflix

DHL – their coverage of SSA is a key component in catalysing eCommerce

Insurance – insurance is finding new markets across Africa and cushioning Africans against shocks that come with the territory. This could need online payment and particularly digital and smart contract based insurance platforms

Local institutions are familiar with local payments market. Local SME’s are growing fast and require a lot of attention and support. Incoming digital commerce can benefit from local legal entity, local compliance, local forex management, protection from the vagaries of internet connectivity, culture, language, legacy systems, local knowledge, local infrastructural instability . . so this is where we can help. Not just a payment provider but as an enabler.

African is a big consumer market with low ATV’s. There are big opportunities for sharing platforms, digital and especially entertainment with COVID, transport and logistics platforms (also COVID-inspired) and a wild card is insurance.

Also successful African eCommerce merchnats seem to have limited understanding and capabilities to set up effective global acquiring for example in Europe and the UK.

Into Africa is card, mobile and EFT and cross border to Europe is mainly card.

The ability for multinational, eCommerce companies in UK and Europe to deal with someone from their home region with African roots makes a difference to their level of understanding and trust levels. In-country acquirers like to deal with their own people and so it works with us having locals on the ground in each country.

The APS strategy of small staff requires a level of outsourcing non-core elements and the choice of leverable business opportunities that require low but very experienced input and value add in exchange for a higher return

So if you are looking for payment at the checkout, and want a team that is very experienced in online payments, click here to give us a shout

I was chatting with my friend Jurgen who is a bleeding edge entrepreneur in the digital currency space about what we can do together in payments and he asked me what I want out of it, which got me thinking.

My thinking is that the industry is going to grow into digital payments over the next 5-10 years and the transition period will involve a lot of on- and off-ramps from fiat to crypto and back. We would like to play that role in the interim.

It would mean a good way for us to continue to expand our “acquiring” footprint. And grow our business and revenues with volumes organically and effortlessly once links are in place and our mutual service expands.

Over time we would like to provide our multinational eCommerce merchants with a simple, seamless and effective traditional and digital payments service. Digital currencies are the future, traditional payments with card, mobile money and bank EFT are legacy . .

Our mission is to bring them together, in the now, to create a new reality.

Personally I would like to see level playing fields for Africa and African’s to simply and easily and effectively participate in the global and digital economy, our focus area being eCommerce – bringing two worlds together to mutual benefit.

Thank you. Please click here if you are looking for payment at the checkout across Africa